Recycled Polyolefin (PO) Blend for Wheeled Trash Can Market Outlook (2026-2034)

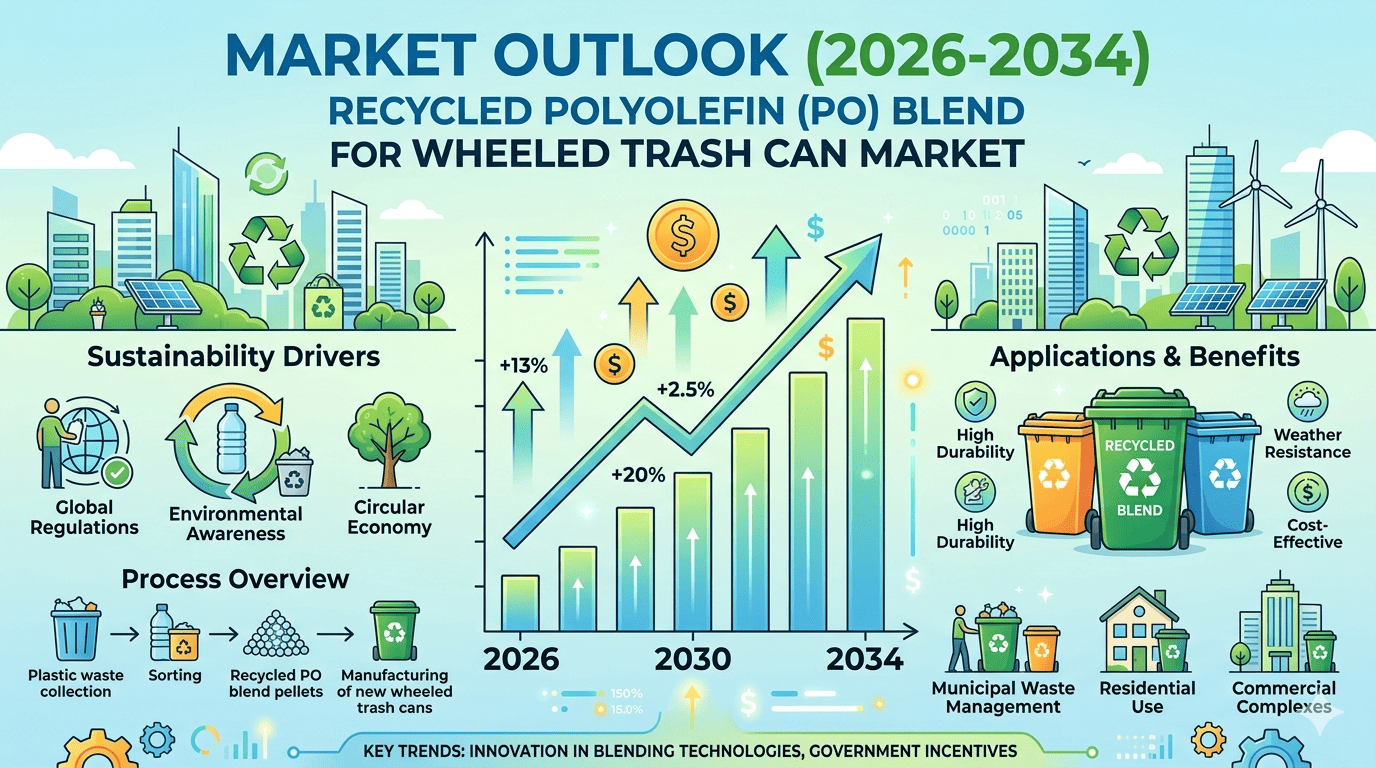

Global Recycled Polyolefin (PO) Blend for Wheeled Trash Can (Injection Molding) market size was valued at USD 1.84 billion in 2025. The market is projected to grow from USD 1.97 billion in 2026 to USD 3.41 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period.

Recycled polyolefin (PO) blends for wheeled trash can injection molding are engineered plastic compounds derived from post-consumer and post-industrial polyolefin waste — primarily recycled polyethylene (rPE) and recycled polypropylene (rPP) — formulated to meet the mechanical and aesthetic demands of large-format waste container manufacturing. These blends are specifically processed to deliver impact resistance, UV stability, and dimensional consistency essential for wheeled refuse bins used in residential, commercial, and municipal applications. What sets this material category apart from other recycled plastics is its practical compatibility with standard injection molding infrastructure, which means manufacturers do not need to overhaul existing equipment to transition toward more sustainable raw material inputs.

The market is witnessing steady momentum driven by increasingly stringent global plastic waste regulations, rising adoption of circular economy principles, and growing municipal procurement mandates that favor products with verified recycled content. Furthermore, advancements in compatibilizer technology and melt-blending processes have significantly improved the performance characteristics of recycled PO compounds, narrowing the quality gap with virgin polyolefins and accelerating their acceptance among injection molders. Key industry participants such as Biffa Polymers, Veolia, ALBA Group, and Plastipak Holdings are actively expanding their recycled resin supply chains to serve this segment.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308927/recycled-polyolefin-blend-for-wheeled-trash-can-market

Market Dynamics:

The market’s trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

-

Rising Regulatory Pressure and Extended Producer Responsibility (EPR) Mandates Accelerating Recycled Content Adoption: Across North America and Europe, governments are increasingly enacting legislation that mandates minimum recycled content thresholds in durable plastic goods, including municipal waste containers. The European Union’s Single-Use Plastics Directive and broader circular economy action plans have created a compliance-driven demand for recycled polyolefin blends in injection-molded applications such as wheeled trash cans. Municipalities procuring large volumes of waste bins for public infrastructure programs are now frequently incorporating recycled content specifications directly into tender requirements, effectively making recycled PO blends not merely a preference but a procurement prerequisite. This regulatory momentum is particularly strong in Germany, France, the Netherlands, and Scandinavian markets, where sustainability criteria are embedded in public procurement frameworks.

-

Cost Competitiveness of Post-Consumer and Post-Industrial Recycled Polyolefins Relative to Virgin Resin: One of the most tangible drivers in this market is the persistent cost advantage that recycled polyolefin blends — particularly those derived from post-consumer high-density polyethylene (HDPE) and polypropylene (PP) — offer compared to virgin resin grades. During periods of elevated crude oil prices, the price differential between recycled and virgin polyolefins has historically widened, incentivizing injection molders of wheeled trash cans to increase recycled content ratios. Manufacturers producing 120-liter, 240-liter, and 360-liter wheeled containers have demonstrated the ability to incorporate between 30% and 80% recycled PO content while maintaining structural integrity and impact resistance specifications required for repeated mechanical collection cycles. This cost lever is especially meaningful for high-volume municipal contract manufacturers operating on thin margins. Furthermore, advancements in compatibilizer chemistry and melt-blending technologies have significantly improved the processability and mechanical output of mixed polyolefin recyclate streams, reducing reliance on highly sorted, single-polymer post-consumer feedstocks. This technical progress has expanded the pool of usable recycled material, stabilized supply chains, and improved the economic case for recycled PO blend use in wheeled container manufacturing.

-

Growing Municipal Infrastructure Spending and Urbanization Driving Volume Demand: Rapid urbanization across emerging economies in Asia-Pacific, Latin America, and the Middle East is generating sustained demand for wheeled waste collection infrastructure. As municipal solid waste management systems are formalized and expanded in cities across India, Brazil, Southeast Asia, and the Gulf Cooperation Council states, procurement of standardized wheeled trash cans — predominantly manufactured via injection molding — is increasing substantially. Local manufacturers in these regions are increasingly adopting recycled polyolefin blends to reduce input costs while meeting growing volume requirements. In parallel, replacement cycles in mature markets such as the United States and Western Europe, where wheeled bin fleets installed over the past two decades require renewal, are creating additional demand waves for injection-molded containers utilizing recycled PO content.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308927/recycled-polyolefin-blend-for-wheeled-trash-can-market

Significant Market Restraints Challenging Adoption

Despite its promise, the market faces hurdles that must be overcome to achieve universal adoption.

-

Limited Availability of High-Quality, Specification-Grade Recycled Polyolefin Feedstock at Commercial Scale: A fundamental structural restraint on market growth is the limited availability of post-consumer recycled polyolefin material that consistently meets the mechanical and rheological specifications required for injection molding of large-format, durable goods such as wheeled trash cans. While global plastic recycling collection volumes have increased, the proportion of post-consumer HDPE and PP that is adequately sorted, cleaned, and processed to a quality suitable for demanding injection molding applications represents a relatively small fraction of total recyclate supply. The majority of available recycled polyolefin is directed toward lower-specification applications such as pipes, film, and non-structural components, leaving a constrained supply of higher-grade material for wheeled container manufacturers. This supply bottleneck limits production scalability and creates price volatility in recycled feedstock markets that complicates long-term cost planning for bin manufacturers.

-

Lack of Harmonized International Standards for Recycled Content Verification and Traceability: The absence of universally adopted, harmonized standards for verifying and certifying recycled content in injection-molded plastic products represents a meaningful market restraint. While certifications such as GRS (Global Recycled Standard) and ISCC PLUS are gaining traction, their adoption across the wheeled trash can supply chain — from recyclate compounder to bin manufacturer to municipal purchaser — remains incomplete and inconsistent across geographies. Without robust mass balance accounting and traceability frameworks, claims of recycled content are difficult for end buyers to verify, limiting the price premium that recycled PO blend products can command and reducing incentives for manufacturers to invest in higher recycled content formulations.

Critical Market Challenges Requiring Innovation

The transition to large-scale commercial production of recycled PO blends for wheeled trash can injection molding presents its own distinct set of challenges that cannot be overlooked. Feedstock quality inconsistency remains the most persistent processing challenge — mixed polyolefin recyclate streams sourced from municipal collection programs frequently contain contamination from food residue, non-polyolefin polymers, adhesives, and colorants, which can negatively affect melt flow index consistency, impact strength, and surface appearance. Injection molding of large-format, thick-walled components demands precise material rheology control, and inconsistent feedstock can lead to sink marks, weld line weaknesses, and dimensional instability, increasing rejection rates and raising per-unit manufacturing costs.

Additionally, color and aesthetic limitations of recycled PO blends create real operational complexity. Post-consumer recycled polyolefins inherently carry a gray or dark brown coloration resulting from mixed pigment streams, limiting achievable color ranges in the final molded part. While wheeled trash cans are generally tolerant of darker, muted colors compared to consumer-facing products, municipal clients increasingly specify consistent color coding — green, blue, brown, or yellow lids — to differentiate waste streams. Achieving uniform, repeatable color in injection-molded bins using high recycled content requires additional pigment loading, adding cost and complexity to bill-of-materials management. Furthermore, the economic case for recycled PO blends is sensitive to crude oil price cycles, and during periods of sustained low oil prices, virgin HDPE and PP resin prices decline, compressing the cost advantage of recycled alternatives and creating cyclical demand uncertainty for compounders.

Vast Market Opportunities on the Horizon

-

Closed-Loop Recycling Programs Between Municipalities and Bin Manufacturers Creating Stable Feedstock Supply Chains: An emerging and strategically significant opportunity lies in the development of closed-loop collection systems in which end-of-life wheeled trash cans are recovered, reprocessed, and reintroduced as feedstock into new bin manufacturing. Several European municipalities and waste management operators have piloted programs in which damaged or obsolete polyolefin wheeled containers are returned to manufacturers or their recycling partners for grinding and recompounding into recycled PO blends used in subsequent production runs. These closed-loop models offer multiple advantages: feedstock composition is known and consistent, contamination levels are significantly lower than open-loop post-consumer streams, and the circular narrative strengthens the sustainability credentials of municipal procurement programs. As circular economy principles become more deeply embedded in public procurement policy, closed-loop bin recycling programs are well-positioned to scale.

-

Advanced Compatibilizer and Additive Technologies Enabling Higher Recycled Content Without Performance Compromise: Continued innovation in compatibilizer chemistry, reactive extrusion processing, and additive stabilization systems presents a substantial opportunity to increase achievable recycled content levels in wheeled trash can injection molding without sacrificing compliance with EN 840 or equivalent performance standards. Specialty chemical companies are actively developing maleic anhydride-grafted polyolefin compatibilizers, reactive impact modifiers, and multifunctional stabilizer packages specifically formulated for mixed post-consumer polyolefin streams. As these technologies mature and achieve wider commercial availability, injection molders will be able to increase recycled content ratios above current thresholds — potentially reaching 90% or higher in bin body components — while maintaining the mechanical durability and UV resistance required for decade-long service life in outdoor municipal environments.

-

Corporate Sustainability Commitments and ESG Reporting Driving Private-Sector Demand for Recycled Content Bins: Beyond the municipal sector, large commercial and retail enterprises are increasingly specifying recycled content in the waste management equipment they procure for store, warehouse, and campus environments as part of commitments to science-based emissions targets and ESG reporting frameworks. Retailers, logistics operators, food service chains, and commercial property managers represent a substantial and growing private-sector demand channel for wheeled waste containers incorporating verified recycled PO content. This segment is attractive because private buyers often demonstrate greater willingness to pay a modest premium for certified recycled content products, providing margin support for manufacturers investing in higher-specification recycled PO formulations. As corporate sustainability reporting requirements become more rigorous — particularly under frameworks such as the EU Corporate Sustainability Reporting Directive — demand from this channel is expected to strengthen progressively through the latter half of this decade.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Recycled High-Density Polyethylene (rHDPE) Blend, Recycled Polypropylene (rPP) Blend, Mixed Recycled Polyolefin (rPO) Blend, and Compatibilizer-Enhanced Recycled PO Blend. Recycled High-Density Polyethylene (rHDPE) Blend stands out as the dominant material type in the wheeled trash can injection molding market owing to its well-established mechanical robustness, excellent impact resistance, and superior dimensional stability under varying load conditions. rHDPE blends are particularly favored by manufacturers seeking a dependable material base that closely mirrors the performance characteristics of virgin HDPE while significantly reducing the carbon footprint of the production process. Recycled Polypropylene blends are also gaining momentum as formulators improve reprocessing technologies to deliver consistent melt flow behavior essential for precision injection molding of large-volume containers.

By Application:

Application segments include Residential Wheeled Trash Cans, Commercial Wheeled Waste Containers, Industrial Wheeled Bins, and others. Residential Wheeled Trash Cans represent the primary application driving demand for recycled polyolefin blends, as municipal solid waste collection programs worldwide continue to mandate or strongly encourage the use of environmentally responsible materials in curbside bin manufacturing. The residential segment benefits from strong government procurement frameworks and green public purchasing policies that compel local authorities to specify recycled-content materials in waste collection infrastructure. Commercial wheeled waste containers deployed in retail, hospitality, and institutional settings represent a growing application area, with facility managers increasingly prioritizing sustainability credentials in procurement decisions.

By End User:

The end-user landscape includes Municipal and Government Bodies, Waste Management Companies, and Commercial and Industrial Enterprises. Municipal and Government Bodies constitute the most influential end-user segment in the recycled polyolefin blend market for wheeled trash cans, as public sector procurement guidelines in numerous countries increasingly mandate minimum recycled content thresholds for waste collection equipment. These institutions drive large-scale, standardized purchasing cycles that reward manufacturers capable of delivering consistent quality across high-volume orders. Waste management companies form a strategically critical end-user group, as they directly operate fleets of wheeled bins and prioritize materials that deliver long operational life, resistance to UV degradation, and ease of maintenance.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308927/recycled-polyolefin-blend-for-wheeled-trash-can-market

Competitive Landscape:

The global Recycled Polyolefin (PO) Blend for Wheeled Trash Can (Injection Molding) market is moderately consolidated and characterized by a mix of large-scale polymer recyclers and compounders supplying reprocessed polyethylene (PE) and polypropylene (PP) blends to municipal waste container manufacturers. Leading the competitive space are established plastics recycling and compounding specialists such as Biffa Polymers (UK) and Veolia Polymers (France), both of which operate dedicated post-consumer and post-industrial polyolefin recycling streams that feed into durable goods applications including injection-molded outdoor containers. These players differentiate themselves through material consistency, contaminant control, and compliance with increasingly stringent recycled content regulations across the EU and North America. Their scale and feedstock access give them a structural advantage in long-term supply agreements with major bin OEMs. The competitive strategy across the market is overwhelmingly focused on securing reliable post-consumer feedstock, investing in advanced sorting and washing technologies, and forming strategic vertical partnerships with end-user companies to co-develop and validate application-specific recycled PO formulations, thereby securing future demand.

List of Key Recycled Polyolefin (PO) Blend Companies Profiled:

-

Biffa Polymers (United Kingdom)

-

Veolia Polymers (France)

-

SUEZ Recycling and Recovery (France)

-

Luxus Ltd. (United Kingdom)

-

KW Plastics (United States)

-

Indorama Ventures Recycling Division (Thailand / Global)

-

MTM Plastics GmbH (Germany)

-

Storopack Recycling (Germany)

The competitive strategy is overwhelmingly focused on securing reliable post-consumer feedstock supply, advancing compounding technology to improve blend performance, and forming strategic vertical partnerships with bin manufacturers and waste management operators to co-develop and validate new application-specific solutions, thereby securing long-term demand.

Regional Analysis: A Global Footprint with Distinct Leaders

-

Europe: Is the undisputed leader in the Recycled Polyolefin (PO) Blend for Wheeled Trash Can market, driven by some of the most stringent regulatory frameworks governing plastic waste and recycled content mandates on the planet. The European Union’s Circular Economy Action Plan and broader Green Deal commitments have compelled municipal authorities and waste management equipment manufacturers across member states to transition toward materials with high post-consumer recycled content. Countries such as Germany, France, the Netherlands, and the Scandinavian nations have developed well-established collection and sorting infrastructure that ensures a consistent and high-quality supply of post-consumer polyolefin feedstock. Public procurement policies in several European countries further reinforce adoption by mandating minimum recycled content in publicly purchased waste collection equipment, creating sustained demand for compliant recycled PO blend products across the region.

-

North America: Represents a significant and growing market, with growth increasingly shaped by evolving state-level regulations in the United States and provincial policies in Canada. While federal mandates on recycled content in durable goods remain less prescriptive than in Europe, a growing number of U.S. states have enacted legislation encouraging or requiring the use of post-consumer recycled materials in municipal procurement. The domestic availability of post-consumer polyolefin streams is improving as curbside collection programs expand and materials recovery infrastructure modernizes. However, price sensitivity and the historical preference for virgin resin-based products continue to present adoption challenges, meaning market penetration of recycled PO blend products is advancing steadily but requires continued policy and supply chain development.

-

Asia-Pacific: Presents a complex and rapidly evolving landscape for recycled polyolefin blends in the wheeled trash can injection molding market. China, as the world’s largest plastics processor, has undergone a significant policy shift following its National Sword initiative, which reshaped global recycled material flows and prompted domestic investment in waste sorting and recycling infrastructure. Growing urbanization across Southeast Asian nations is driving increased demand for waste collection equipment, including wheeled trash cans, although the penetration of recycled PO blends varies considerably by country based on local regulatory frameworks and feedstock availability. Japan and South Korea maintain mature recycling ecosystems and strong environmental policy commitments that support the use of recycled materials in municipal equipment.

-

South America and Middle East & Africa: These regions represent the emerging frontier of the Recycled Polyolefin (PO) Blend for Wheeled Trash Can market. While currently smaller in scale, they present significant long-term growth opportunities driven by increasing urbanization, expanding municipal waste management infrastructure investments, and a growing policy focus on circular economy principles. Brazil, as the largest economy in South America, is gradually expanding its formal recycling sector supported by national solid waste legislation, while Gulf Cooperation Council countries in the Middle East are beginning to embed sustainability procurement priorities into national vision plans. Until domestic recycling infrastructure investment catches up with waste generation growth in these geographies, adoption of recycled PO blends will advance more gradually.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308927/recycled-polyolefin-blend-for-wheeled-trash-can-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308927/recycled-polyolefin-blend-for-wheeled-trash-can-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/