Cyanoacrylate (CA) Instant Adhesive for Medical Skin Closure Market Outlook (2026-2034): Growth Fueled by Sutureless Surgical Technologies and Advanced Wound Care Adoption

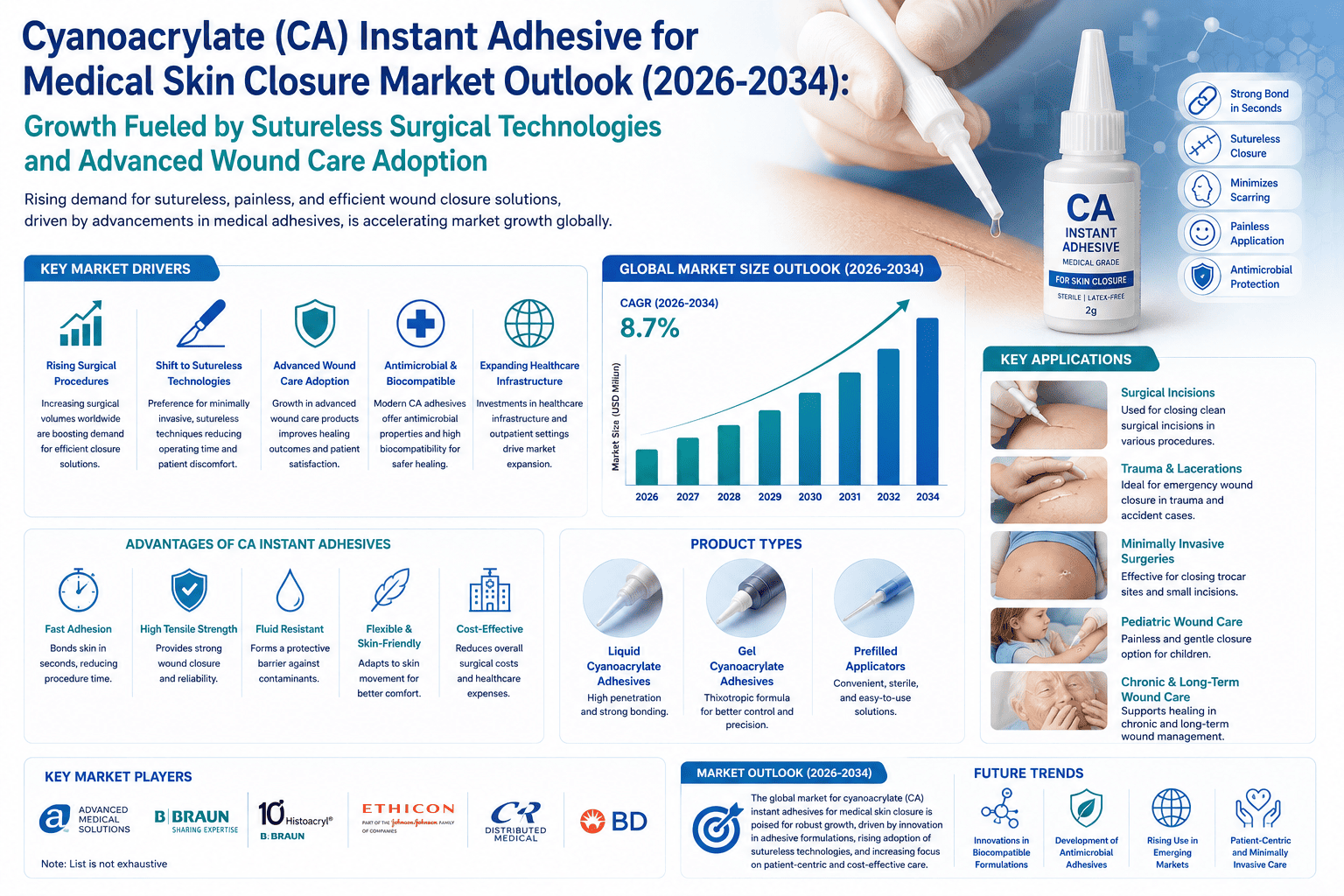

Global Cyanoacrylate (CA) Instant Adhesive for Medical Skin Closure (Dermabond) market size was valued at USD 412.6 million in 2025. The market is projected to grow from USD 441.8 million in 2026 to USD 798.5 million by 2034, exhibiting a remarkable CAGR of 7.7% during the forecast period.

Cyanoacrylate-based medical skin closure adhesives, widely recognized under the brand name Dermabond, are topical skin adhesives used as an alternative to sutures, staples, and adhesive strips for closing surgical incisions and traumatic lacerations. These fast-polymerizing compounds bond tissue surfaces upon contact with moisture, forming a flexible, waterproof film that holds wound edges together while simultaneously providing a microbial barrier. Products in this category include 2-octyl cyanoacrylate and n-butyl cyanoacrylate formulations, differentiated by viscosity, tensile strength, and intended clinical application. The inherent chemistry of cyanoacrylate adhesives—characterized by rapid anionic polymerization triggered by trace amounts of water on the skin surface—makes them uniquely suited for medical skin closure in a way that no conventional wound closure method can fully replicate.

The market is gaining meaningful traction owing to the rising volume of surgical procedures globally, growing preference for minimally invasive wound closure techniques, and increasing awareness among healthcare providers regarding the clinical and cosmetic advantages of tissue adhesives over traditional suturing. Furthermore, the ability of CA-based adhesives to reduce procedure time and lower infection risk continues to drive their adoption across emergency departments, ambulatory surgical centers, and dermatology practices. Ethicon Inc. (a Johnson & Johnson company), Chemence Medical, and Medline Industries are among the prominent players actively shaping the competitive landscape with differentiated product portfolios.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308770/cyanoacrylate-instant-adhesive-for-medical-skin-closure-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities that manufacturers and investors are only beginning to fully appreciate.

Powerful Market Drivers Propelling Expansion

-

Rising Demand for Minimally Invasive and Sutureless Wound Closure Solutions: The cyanoacrylate instant adhesive market for medical skin closure has experienced sustained momentum driven by the growing clinical preference for sutureless wound management. Cyanoacrylate-based tissue adhesives such as 2-octyl cyanoacrylate—widely recognized under the brand name Dermabond—have demonstrated comparable or superior outcomes to traditional sutures and staples across a range of superficial laceration and surgical incision closures. These adhesives polymerize rapidly upon contact with skin moisture, forming a strong, flexible bond that eliminates the need for needle penetration, thereby reducing patient discomfort, cutting procedure time, and lowering the risk of needlestick injuries among healthcare workers. Emergency departments, outpatient surgical centers, and pediatric care units have increasingly adopted these products precisely because of their ease of application and the reduced anxiety they generate in patients, particularly children.

-

Expansion of Ambulatory Surgical Centers and Outpatient Care Settings: A significant structural shift in healthcare delivery—from inpatient hospital settings toward ambulatory surgical centers (ASCs) and outpatient clinics—has created a highly favorable environment for cyanoacrylate skin closure products. Procedures performed in ASCs typically prioritize rapid patient turnover, reduced complication rates, and efficient wound management protocols, all of which align closely with the clinical profile of CA adhesives. These settings benefit from the adhesive's ability to act as a microbial barrier, reducing postoperative infection risk without the requirement for suture removal follow-up appointments. As healthcare systems globally continue to manage capacity pressures and cost constraints, the operational advantages of tissue adhesives over conventional closure methods translate into measurable and demonstrable efficiencies. This shift has been particularly pronounced in North America and Western Europe, where outpatient procedure volumes have grown substantially over the past decade.

-

Aging Global Population and Rising Incidence of Chronic Surgical Conditions: The demographic reality of an aging global population has amplified demand for wound closure solutions suited to fragile or compromised skin. Elderly patients often present with tissue that is poorly suited to conventional suturing, making the gentle application and flexible bond of CA adhesives particularly appropriate for their clinical management. Simultaneously, the rising incidence of chronic conditions requiring surgical intervention—including cardiovascular disease, diabetes-related complications, and orthopedic disorders—continues to expand the total addressable patient population for medical skin closure products. These converging demographic and epidemiological trends serve as durable, long-term structural drivers for the cyanoacrylate skin adhesive market, providing a foundation of sustained demand that is unlikely to erode over the forecast horizon.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308770/cyanoacrylate-instant-adhesive-for-medical-skin-closure-market

Significant Market Restraints Challenging Adoption

Despite its compelling clinical promise, the market faces real and substantive hurdles that must be acknowledged and systematically addressed before universal adoption can be achieved across all care settings and geographies.

-

Tissue Toxicity Concerns and Formulation Constraints Limiting Product Development: A well-documented restraint on the cyanoacrylate skin adhesive market is the cytotoxic potential associated with shorter-chain CA monomers, particularly methyl and ethyl cyanoacrylate formulations. These compounds degrade to release cyanoacetate and formaldehyde as byproducts—substances that can provoke localized tissue irritation, inflammatory responses, and delayed wound healing when present in sufficient concentrations. As a result, the medical-grade segment has gravitated toward longer-chain formulations such as 2-octyl cyanoacrylate, which exhibit lower degradation rates and improved tissue compatibility. However, these longer-chain variants present their own manufacturing challenges, including greater viscosity and more complex polymerization kinetics, which constrain the range of achievable product configurations and application formats.

-

Cost Sensitivity in Price-Constrained Healthcare Markets: Cyanoacrylate skin adhesives carry a higher per-unit cost compared to traditional suture materials and staples. In healthcare systems operating under tight reimbursement frameworks—particularly in emerging economies and public health institutions in lower-income countries—procurement decisions are heavily influenced by direct cost comparisons. While the total cost of care argument, which accounts for reduced follow-up visits, shorter procedure times, and lower infection rates, can justify the premium pricing of CA adhesives, this analysis is not always systematically applied in institutional purchasing decisions. Budget-constrained hospitals and clinics may default to suture-based closure as a cost-containment measure, even where clinical guidelines would support adhesive use. This price sensitivity creates a structural barrier to volume growth in markets where reimbursement for wound closure products is limited or non-existent.

Critical Market Challenges Requiring Innovation

The clinical limitations of cyanoacrylate adhesives present real operational challenges that manufacturers and clinicians are working together to address. CA adhesives are clinically indicated primarily for low-tension, superficial lacerations and incisions where wound edges can be approximated without significant mechanical stress. They are generally contraindicated in wounds over joints with high mobility, deep puncture wounds, animal bites, infected wounds, and areas with dense hair. This inherent anatomical and wound-type specificity limits the proportion of total wound closure procedures in which these products can be substituted for sutures or staples. Clinicians must exercise careful patient selection, and misapplication in inappropriate wound contexts can result in wound dehiscence, adhesive failure, or delayed healing—outcomes that, while relatively uncommon when protocols are followed, can generate reluctance among providers less familiar with the technology.

Additionally, the regulatory pathway for medical-grade cyanoacrylate adhesives is more demanding than for industrial or over-the-counter formulations, requiring clinical evidence of safety and efficacy, biocompatibility testing, and conformance with medical device regulations in each target market. For manufacturers seeking to enter or expand within regulated markets such as the United States, the European Union, and Japan, these requirements represent substantial barriers in terms of time and investment. Furthermore, because the core chemistry of cyanoacrylate adhesives is well-established, meaningful product differentiation is difficult to achieve, creating competitive pressure on pricing and margins.

Vast Market Opportunities on the Horizon

-

Innovation in Formulation Technology and Next-Generation Adhesive Development: Significant commercial opportunity exists for manufacturers capable of advancing beyond the current generation of cyanoacrylate adhesive formulations. Research efforts focused on hybrid adhesive systems—which combine the rapid polymerization of cyanoacrylates with the flexibility of polyurethane or silicone components—aim to address the tension-resistance limitations that currently restrict CA adhesive use over mobile anatomical sites such as joints and the face. Additionally, the incorporation of antimicrobial agents, wound-healing biologics, or drug-eluting compounds into the adhesive matrix represents an actively explored frontier with the potential to transform tissue adhesives from passive closure devices into active therapeutic platforms. Companies that successfully navigate the regulatory pathway for such combination products could access substantially higher reimbursement tiers and establish meaningful differentiation in an otherwise commoditizing market segment.

-

Expansion into High-Growth Emerging Markets Through Affordable Product Strategies: Emerging economies across Asia-Pacific, Latin America, the Middle East, and Africa represent a substantial and underserved opportunity for the cyanoacrylate skin adhesive market. Rapidly expanding healthcare infrastructure, growing surgical procedure volumes, rising middle-class populations with increasing access to formal healthcare, and government initiatives to upgrade wound care standards are collectively creating the conditions for accelerated adoption. Manufacturers that develop cost-optimized product variants—potentially through localized manufacturing partnerships, tiered pricing strategies, or the introduction of smaller unit-dose formats suited to lower-volume procedure settings—could capture meaningful market share in these geographies before competitive dynamics intensify.

-

Increasing Utilization in Veterinary Medicine and Adjacent Clinical Applications: Beyond the core human medical market, cyanoacrylate adhesives are finding growing application in veterinary surgical practice, where the demand for efficient, sutureless wound closure in animal patients is expanding alongside the broader premiumization of companion animal healthcare. The veterinary segment, while smaller in absolute terms, represents a less regulated and faster-moving adoption environment where clinical uptake can be driven by individual practitioner preference. Additionally, emerging evidence supporting the use of CA adhesives in specialized human clinical applications—including securing peripheral intravenous catheters and managing mucosal tears in select endoscopic procedures—opens incremental market segments that could collectively contribute meaningfully to total market expansion over the coming decade.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into 2-Octyl Cyanoacrylate, N-Butyl Cyanoacrylate, Methyl Cyanoacrylate, Ethyl Cyanoacrylate, and others. 2-Octyl Cyanoacrylate currently leads the market, favored for its superior flexibility, longer chain molecular structure, and significantly reduced tissue toxicity compared to shorter-chain variants. Its enhanced bonding strength and biocompatibility make it particularly well-suited for use on skin surfaces that experience frequent movement and tension, cementing its position as the gold standard formulation across clinical settings globally. N-Butyl Cyanoacrylate maintains a notable secondary presence, especially in cost-sensitive markets and applications requiring rapid polymerization.

By Application:

Application segments include Surgical Wound Closure, Traumatic Laceration Closure, Cosmetic and Reconstructive Procedures, Emergency and Acute Care, and others. The Surgical Wound Closure segment currently dominates, driven by the strong and sustained preference among surgeons for post-operative incision management solutions that reduce procedure time, eliminate the need for suture removal appointments, and provide a reliable microbial barrier throughout the healing phase. However, the Traumatic Laceration Closure and Cosmetic and Reconstructive Procedures segments are expected to exhibit the highest growth rates in the coming years, reflecting broadening clinical acceptance.

By End User:

The end-user landscape includes Hospitals and Surgical Centers, Ambulatory Surgical Centers (ASCs), Emergency Clinics and Urgent Care Centers, and Dermatology and Cosmetic Clinics. Hospitals and Surgical Centers constitute the dominant end-user category, driven by the high volume of surgical procedures performed and the critical importance of reliable wound management protocols in these settings. However, Ambulatory Surgical Centers are emerging as a rapidly growing end-user group, propelled by the global trend toward outpatient procedures and same-day discharge models where faster wound closure methods are operationally advantageous.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308770/cyanoacrylate-instant-adhesive-for-medical-skin-closure-market

Competitive Landscape:

The global Cyanoacrylate (CA) Instant Adhesive for Medical Skin Closure market is characterized by a concentrated group of established medical device manufacturers alongside a growing number of specialized regional players competing on clinical performance, regulatory approvals, and cost-effectiveness. The top three companies—Ethicon, Inc. (Johnson & Johnson, U.S.), Chemence Medical, Inc. (U.S.), and Medline Industries, LP (U.S.)—collectively command a significant share of the global market. Their dominance is underpinned by extensive clinical evidence portfolios, well-established reimbursement pathways, advanced production capabilities, and strong brand recognition among surgeons and emergency medicine physicians across major healthcare markets worldwide.

Beyond the market leaders, a number of specialized manufacturers have carved out competitive positions by targeting specific clinical segments, geographies, or cost-sensitive markets. Competition at all tiers is driven primarily by clinical data differentiation, formulation innovation—including antimicrobial and colored variants for enhanced visualization during application—and long-term supply agreements with integrated health systems and group purchasing organizations. The competitive strategy across the board is overwhelmingly focused on R&D to enhance product quality and broaden clinical applicability, alongside forming strategic vertical partnerships with end-user institutions to co-develop and validate new applications, thereby securing durable future demand.

List of Key Cyanoacrylate Medical Skin Closure Companies Profiled:

-

Ethicon, Inc. (Johnson & Johnson) (United States)

-

Medline Industries, LP (United States)

-

Cardinal Health, Inc. (United States)

-

Chemence Medical, Inc. (United States)

-

GluStitch Inc. (Canada)

-

Aesculap AG (B. Braun) (Germany)

-

Adhezion Biomedical, LLC (United States)

-

Henkel AG & Co. KGaA (Germany)

The competitive strategy across the cyanoacrylate medical skin closure market is overwhelmingly focused on R&D investment to enhance formulation performance, expand clinical indications, and reduce manufacturing costs, alongside forming strategic partnerships with hospital systems, group purchasing organizations, and clinical research institutions to co-develop and validate new applications, thereby securing long-term demand.

Regional Analysis: A Global Footprint with Distinct Leaders

-

North America: Is the undisputed leader in the global Cyanoacrylate (CA) Instant Adhesive for Medical Skin Closure market. This dominance is fueled by a well-established healthcare infrastructure, high procedural volumes, favorable reimbursement frameworks established by the U.S. Food and Drug Administration, and strong adoption of advanced wound closure technologies across emergency departments, surgical suites, and outpatient care facilities. The presence of key market participants and ongoing investments in clinical research further strengthen North America's leading regional position.

-

Europe & Asia-Pacific: Together, they form a powerful and growing secondary bloc. Europe's strength is driven by mature healthcare systems in Germany, the United Kingdom, France, and Italy, supported by CE marking oversight and a growing emphasis on reducing hospital-acquired infections and shortening post-operative recovery periods. Asia-Pacific is emerging as one of the fastest-growing regions, propelled by rapid improvements in healthcare infrastructure, expanding access to advanced medical products, rising surgical procedure volumes in China, Japan, India, and Australia, and increasing healthcare expenditure by governments across the region.

-

South America and Middle East & Africa: These regions represent the emerging frontier of the cyanoacrylate medical skin closure market. While currently smaller in scale, they present significant long-term growth opportunities driven by expanding private healthcare sectors, increasing procedural volumes in urban centers, growing urbanization, and ongoing investments in healthcare infrastructure modernization. South America is led by Brazil and Argentina, while Gulf Cooperation Council countries, particularly the United Arab Emirates and Saudi Arabia, lead adoption across the Middle East and Africa.

Get Full Report Here: https://www.24chemicalresearch.com/reports/308770/cyanoacrylate-instant-adhesive-for-medical-skin-closure-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/308770/cyanoacrylate-instant-adhesive-for-medical-skin-closure-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/