What Homeowners Should Know Before You Buy a Home Before Selling

When you want to buy a home before selling your current one, the transaction sequence that feels natural creates a problem most homeowners don't see until they're already in it.

You find the home you want. You're ready to make an offer. Then the question arrives: how do you commit to buying before you know what your current home will sell for? The two transactions are connected, and the conventional approaches for managing that connection both carry costs that show up at the worst possible moment.

This guide covers what Seattle homeowners need to know before they attempt to buy a home before selling, including the program that resolves the problem before the offer is ever submitted.

The Two Default Options and Why Both Create Problems

Most homeowners who want to buy home before selling land on one of two approaches. Both are widely used. Both transfer risk rather than resolve it.

What Contingent Offers Cost Buyers in Seattle

A contingency offer attaches a condition to the new purchase: the deal closes only if the current home sells first. From the buyer's side, it feels like a reasonable safeguard. From the seller's side, it introduces a variable they have no control over.

Seattle sellers in competitive neighborhoods receive multiple offers. When a contingent offer arrives alongside cleaner bids, the contingency becomes the deciding factor. The seller doesn't know the buyer's current home. They don't know its condition, its price, or whether it will attract offers quickly. Accepting a contingent offer means holding the property while waiting on a second transaction they can't monitor or influence.

Most sellers don't accept that uncertainty when they don't have to.

The Kick-Out Clause Risk

Sellers who do accept contingent offers typically retain the right to continue marketing the property. If a better offer arrives, the original buyer gets a short window to remove the contingency or lose the deal. That's the kick-out clause, and it puts the buyer back under pressure at exactly the moment they need stability.

Removing the contingency under a kick-out deadline means committing to the purchase before the current home is sold, which is the problem the contingency was meant to solve. The buyer ends up in a worse position than if they'd structured the offer differently from the start.

What Bridge Loans Actually Add to the Transaction

When homeowners realize they need down payment funds before the current home sells, a bridge loan is usually the first alternative they consider. A bridge loan provides short-term access to existing equity to cover the gap.

The costs are real. Bridge loans carry interest from day one, require monthly payments during the period both properties are held, and show up as a new debt obligation on the buyer's financial profile. That debt-to-income impact arrives at exactly the moment the buyer needs their qualification to look cleanest for the new purchase.

Lenders reviewing the new purchase application see the bridge loan balance and the monthly payment. That affects how much the buyer qualifies for and, in some cases, whether they qualify at all. The solution to one problem creates another one directly downstream.

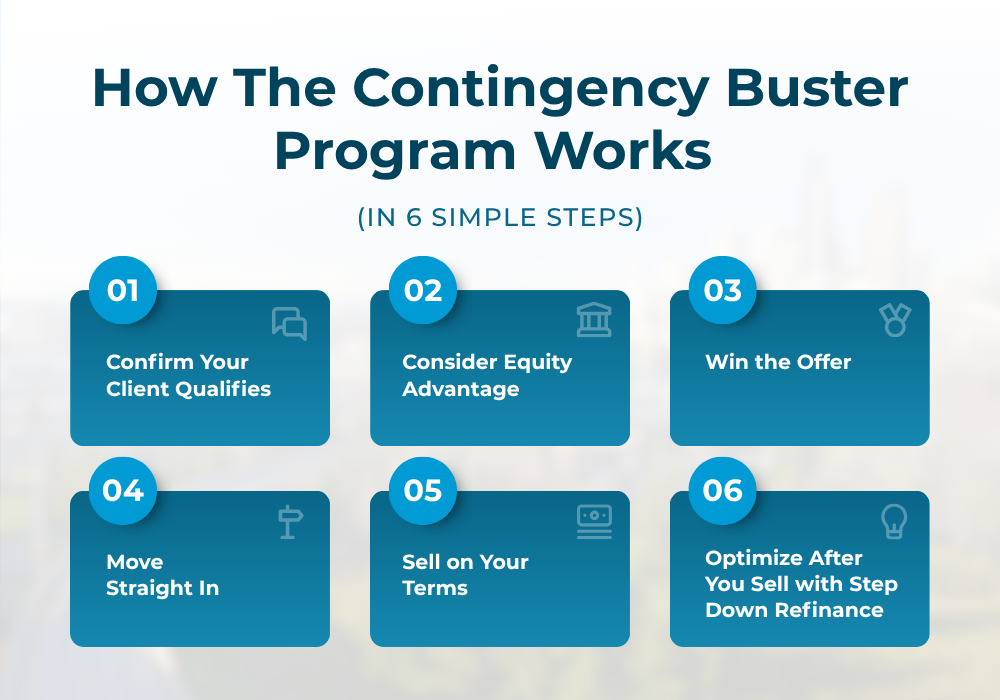

How the Contingency Buster Program Lets You Buy a Home Before Selling

The Contingency Buster Program from Seattle's Mortgage Broker is built specifically for homeowners who want to buy a home before selling without a contingency attached to the new offer and without a bridge loan straining the qualification.

The program resolves the core problem from a different direction. Instead of asking the seller to absorb uncertainty about the current home's sale, the sale is committed before the new offer is written.

The Equity Threshold That Activates the Program

Qualifying for the Contingency Buster Program starts with confirming the equity position in the current home. A minimum equity threshold is required, and Seattle's Mortgage Broker confirms that threshold in the first conversation.

Equity confirmation isn't just a qualification check. It's the foundation everything else is built on. The confirmed equity position determines whether the guaranteed backup purchase contract is available, how much can be accessed through the Equity Advantage Program for the down payment, and what the offer on the new home can look like structurally.

Homeowners who skip this step and begin searching for a new home before confirming their equity position often find themselves mid-search with financing that doesn't support the offer they need to make. Starting with equity confirmation keeps the entire process on a predictable timeline.

What a Guaranteed Backup Purchase Contract Does for the Offer

Once the equity threshold is confirmed, Seattle's Mortgage Broker secures a guaranteed backup purchase contract on the current home. This is a committed buyer already in place before the homeowner enters the market for the next property.

The distinction between a guaranteed contract and a standard listing matters here. A listing puts the home on the market and waits. Offers may come quickly or they may not. The timeline and the final price are unknown until the market responds. None of that uncertainty can be resolved before the buyer needs to make a competitive offer on the next property.

A guaranteed backup purchase contract commits a buyer to the current home on defined terms before the search for the next home begins. The sell-first condition has nothing to solve for because the sale is already committed. The new offer goes in without the contingency attached.

Funding the Down Payment Through Equity Advantage

With a guaranteed buyer committed to the current home, the next question is where the down payment comes from before that sale closes.

The Equity Advantage Program answers that question without adding monthly debt obligations to the buyer's financial profile.

Accessing Equity Before the Sale Closes

Equity Advantage provides access to existing home equity before the current home sells. The advance can be used toward the down payment on the new home, closing costs, staging expenses, moving costs, or debt payoff that strengthens the qualification profile for the new purchase.

The program functions differently from a bridge loan in one critical way: no monthly payment is required while both properties are held. The advance sits against the current home's equity and is repaid in full through escrow when that home closes. The buyer carries the advance without it showing up as an active monthly obligation on the new purchase qualification.

No Monthly Payments and What That Means for Qualification

The debt-to-income ratio is one of the primary factors lenders evaluate when qualifying a buyer for a new purchase. A bridge loan adds a monthly payment to that ratio at exactly the wrong moment. Equity Advantage doesn't.

Because no monthly payment is required on the advance, the buyer's debt-to-income ratio stays exactly where it needs to be for the new purchase qualification to remain clean. The down payment is fully funded. The qualification profile is unaffected. The offer on the new home reflects a buyer whose finances are stable, not a buyer managing two debt obligations simultaneously.

What the Offer Looks Like When You Buy a Home Before Selling

At this point in the process, the variables that typically weaken a buy-before-sell offer have been resolved.

Equity is confirmed. A guaranteed buyer is committed to the current home. The down payment is fully funded through Equity Advantage with no monthly payment impact on the qualification. The offer reflects that preparation.

How a Contingency-Free Offer Reads to a Seattle Seller

No home sale contingency. No sell-first clause. No language in the offer that signals the transaction depends on a second sale completing first. The seller receives a fully funded purchase offer from a buyer whose current home already has a committed buyer in place.

Seattle sellers evaluate offers on two criteria: price and certainty of closing. Cash offers have historically dominated the certainty side of that equation. A buyer who has secured a guaranteed backup purchase contract on their current home and funded their down payment through Equity Advantage arrives at the new offer in a structurally comparable position. The offer is financed, but it carries none of the uncertainty that typically separates financed buyers from cash buyers in a multiple-offer situation.

Sellers who have previously dealt with contingent offers falling through understand exactly what that uncertainty costs them. When a clean, fully funded offer arrives without conditions attached, it stands out in a way that price alone rarely achieves.

Closing Timeline and the Direct Move Outcome

Seattle's Mortgage Broker moves through underwriting quickly, keeping the file ready well before the legal two-week minimum close window.

By law, a primary residence cannot close in under two weeks, but that wait runs on the clock, not on the buyer's file. The paperwork is ready. The timeline runs its course.

End-of-Month Timing

Timing the close at the end of the month eliminates mortgage payment overlap. Closing at month-end means the first payment on the new home doesn't arrive until the following cycle. Any overlap with the current mortgage is avoided, and the monthly budget stays clean during the transition.

One Move, No Storage

Once the close is complete, the move is direct. No storage unit. No short-term rental. No period where two households are running simultaneously with costs attached to both. The new home is ready and the move happens once.

Why Moving First Puts You in a Better Position When You Sell Your Current Home

Moving into the new home first changes how your current property goes to market. That change has a direct impact on what your home sells for.

Why Vacant and Staged Homes Sell Stronger

A lived-in home sold under deadline pressure performs differently than a vacant, professionally staged property with no timeline forcing the seller's hand.

Staged homes sell faster and command stronger offers than comparable unstaged properties. Personal items, furniture arrangements built for living rather than showing, and the general evidence of daily occupation all affect how buyers experience a home during a showing. A vacant, staged property lets buyers see the home itself. The current owner's version of the space doesn't compete with what the buyer is trying to picture.

On a Seattle home, even a modest premium from professional staging represents meaningful equity. That equity follows the seller directly into the financial picture of the new home.

Selling after moving out also means repairs and touch-ups can be completed without working around an occupied household. The property goes to market in its best condition, not the condition manageable while a family is still living in it.

How Selling Without a Deadline Changes the Final Price

Deadline-driven sellers accept the first reasonable offer because waiting carries a financial cost. Every week the current home sits unsold is a week the seller is managing transition pressure.

Homeowners who have already moved into the new home don't carry that pressure. The current property is vacant, staged, and generating showing activity without a countdown running. If the first offers don't reflect the home's value, the seller can hold. That position consistently produces stronger final sale prices than selling under a deadline.

How to Apply Your Sale Proceeds Through the Step Down Refinance Program

When the current home closes, the proceeds don't have to sit idle. Equity from the sale can be applied directly to the new mortgage balance through Seattle's Mortgage Broker's Step Down Refinance Program.

A lower balance creates the conditions for a refinance that reduces the interest rate and the monthly payment without adding loan costs back onto the balance. Traditional refinances carry Total Loan Costs that get added to the loan balance each time they're used. Stack two or three refinances and those accumulated costs offset a meaningful portion of the rate savings.

The Step Down Refinance Program zeroes out or refunds Total Loan Costs at closing. What can't be waived gets refunded directly to the client. The loan balance doesn't grow when the rate drops. After six on-time payments, the program is available again. Each rate drop becomes an opportunity to act without paying the entry cost that makes traditional refinancing expensive to repeat.

What started as a decision to buy home before selling becomes a long-term interest reduction strategy built directly into the mortgage structure from day one.

Take the Next Step Toward Buying a Home Before Selling in Seattle

Buying before selling isn't the complicated, high-risk move most homeowners assume it is.

With the right program behind you, the sequence becomes straightforward and the outcome is better on both ends of the transaction.

If you're sitting on equity in your current home and you've found a neighborhood you want to be in, that's enough to have a real conversation.

Connect with Seattle's Mortgage Broker to find out if you qualify and what your path forward looks like from where you stand today.

Frequently Asked Questions About How to Buy a Home Before Selling

What Equity Do I Need to Qualify?

Seattle's Mortgage Broker confirms the minimum threshold in the first conversation. If the current home qualifies, the guaranteed buyer contract, Equity Advantage funding, and contingency-free offer all become available.

Do I Carry Two Mortgages at the Same Time?

No. The Equity Advantage advance covers the down payment with no monthly payment obligation and repays automatically through escrow when the current home closes.

How Long Does the Process Take?

Underwriting typically completes in under a week. The legal minimum close on a primary residence is two weeks, and most transactions close within that window after offer acceptance.

What Happens If the Current Home Takes Longer to Sell?

The guaranteed backup purchase contract commits a buyer before the new offer is submitted, so the close follows the contract terms regardless of broader market conditions.

Does This Work in Seattle's Competitive Market?

The program was built for Seattle's market specifically because contingent offers lose in multiple-offer situations. Removing the sell-first condition before the offer is submitted is what changes the outcome.